The true cost of low-cost payment providers

July 29, 2024

Payments strategy

Every industry has low-cost providers, and they’re not all terrible. Every day, as consumers and in business, we weigh the cost of different products and decide if the lower-cost option is “good enough”.

Payment providers are no different… to a point. While the highest-cost provider isn’t necessarily the best, no one becomes the lowest-cost provider without compromising on quality or service.

These compromises have material consequences that often outweigh the superficial savings.

As a software company, you have an obligation to choose the right payments partner and negotiate a fair price. But below a certain price point, payment providers aren’t giving you a good deal. They’re quoting a price at which they literally can’t afford to support you as a customer. In this case, the software company ultimately pays the price.

How SaaS companies can grow revenue with embedded payments

Payment provider cost is one of three variables that determine how much a software company profits from embedded payments.

Price to merchants

The first variable is price to merchants. If merchants pay 3.9%, there’s a lot more revenue in play than if merchants pay 2.9%.

Interchange passthrough

The second variable is interchange passthrough. This includes the interchange fees (determined by card networks and paid to issuing banks) and network dues, fees, and assessments. In industries with significant B2B payment volume, software companies can often reduce interchange by 20 - 30 basis points by sending additional data with the transactions and enrolling qualified merchants in special programs.

Payment provider fees

These are fees, including buy-rate and revenue share, that the payment provider deducts after paying interchange passthrough and before distributing residuals to the software platform.

When optimizing for profit, these are the three “levers” that platforms can adjust to earn more money. Choosing a low-cost provider may minimize payment provider fees (even low-cost providers often have hidden fees), but can force platforms to compromise on interchange optimization and merchant pricing.

Unsustainable pricing

When payment providers lead with low pricing, they’re speculating. It’s like buying thousands of lottery tickets with the hope that one will hit the jackpot. In this case, the payment provider is hoping that, if they board enough software platforms with low unit economics, one of those platforms will be a unicorn and the processing volume from that unicorn will generate enough revenue to pay the bills.

The reality, behind the scenes, is that the payment provider isn’t bringing in enough revenue to properly support their product or the software platforms they’re boarding. In the short term, rock bottom pricing can feel like a win for software platforms. In the long run, the payment provider doesn’t have enough funds to deliver on its commitments, and the software company is the one buried in support tickets due to underlying payments product issues, dealing with a new account manager every few months, and either facing a drastic price increase when the payment provider tries to right the ship or executing another payments integration and migration so they can change providers again.

Product issues

We talked with a software platform that initially chose a low-cost payment provider because of lower payment processing cost, lower POS device cost, and an assortment of more than 20 different POS devices to choose from.

Once this platform started implementing, they were offered a choice of only one POS device (the platform was expecting a selection of 20 devices). That device had connectivity issues, and couldn’t consistently perform the one task that POS devices are expected to do – processing payments.

Every story is slightly different, but the theme is consistent. The product doesn’t work quite the way it should. Deposit reports are a little off. 3DS fails more often than it should. Interchange rates are reported or categorized incorrectly. A few API events don’t send webhooks.

Payment processing requires accuracy and reliability. If the data from your payments provider is right 80% of the time, it might as well be wrong all the time.

While it’s possible to build manual workarounds to compensate for product issues, this significantly increases support needs and technical complexity. Payment provider product issues are a shaky foundation and, like creaky doors in a sinking house, they almost always cause problems in the merchant-facing payments experience.

Lack of support

When payment providers aren’t bringing in enough revenue, support is one of the first functions to lose resources.

Since payment processing is a business-critical function, inadequate support from the payment provider is a massive risk to every software company that relies on them. Even the most sophisticated software companies partnering with the best payment providers will still need support sometimes, and inadequate support has very real consequences:

- Slow merchant onboarding

- Delays in fraud review or releasing funds

- Getting stuck with rigid, default configurations

A provider without enough support resources is going to take longer to respond to routine payment operations support needs.

A provider with product issues and inadequate support resources is going to take even longer, because the support demands are amplified by the product issues.

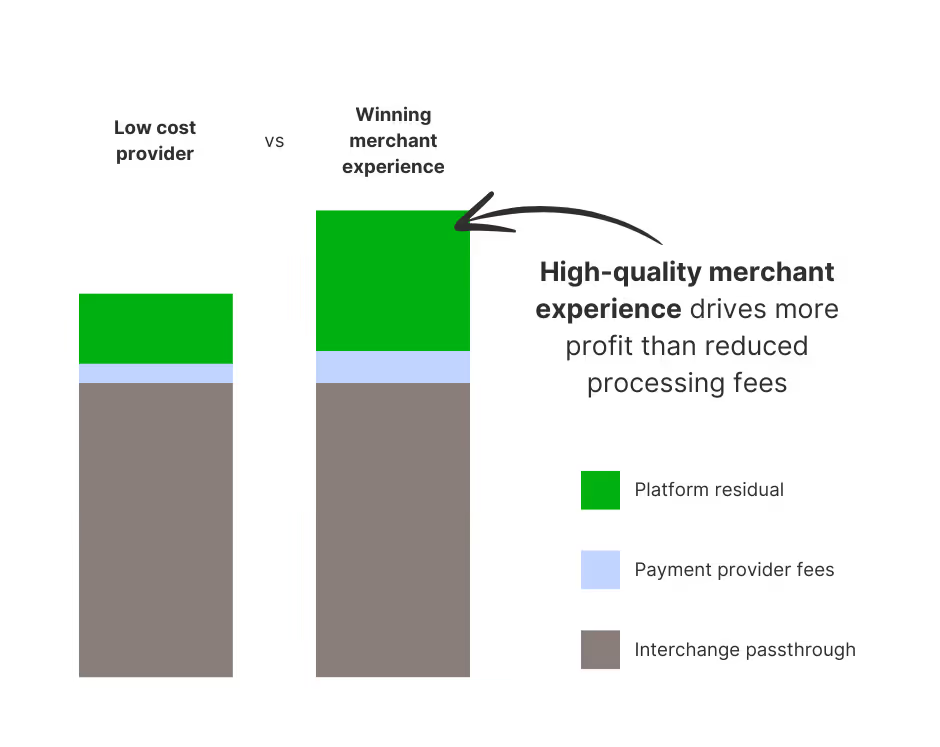

Product issues and lack of support lead to a frustrating and disjointed merchant experience, which prevents software companies from charging premium prices. In extreme cases, it can even force software companies to discount payment processing to retain unhappy merchants. When the platform can’t offer a great merchant experience, the opportunity costs of a low-cost payment provider far outweigh the superficial savings.

Furthermore, a provider who isn’t bringing in enough revenue to invest in their core support team certainly can’t invest in subject matter experts who assist software platforms with more advanced payments strategy, like optimizing interchange and driving adoption.

Lack of interchange optimization

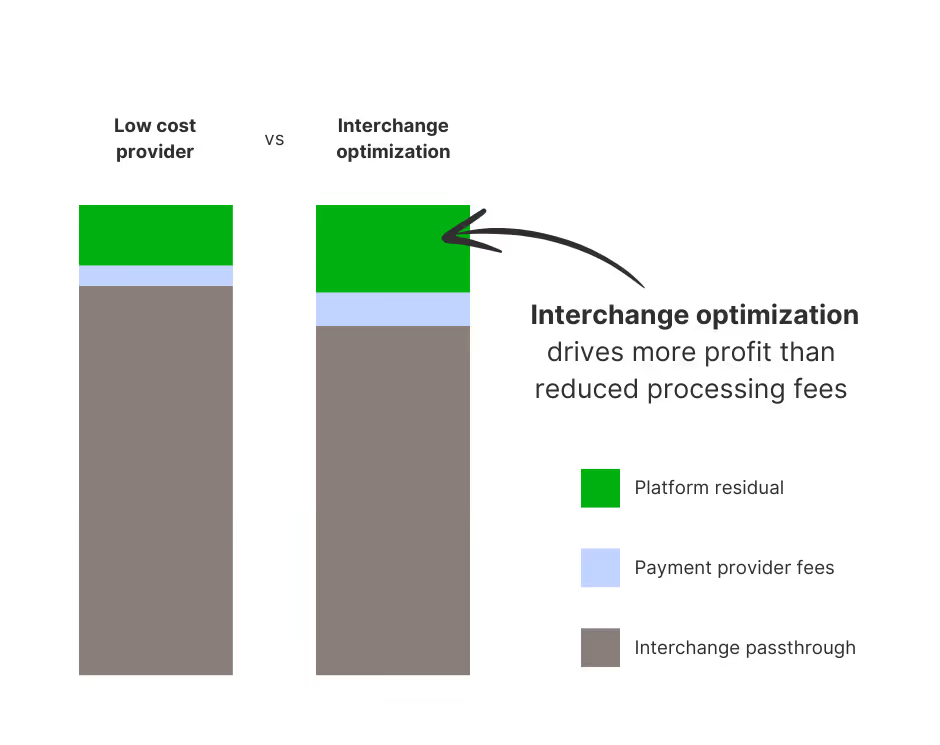

Most payment providers can send Level 2 and Level 3 data. What they don’t say is that sending Level 2 and Level 3 data does not guarantee that transactions will actually qualify for lower interchange rates.

For example, we work with a software platform who was passing Level 2 and Level 3 data but most transactions weren’t qualifying for Level 2 and Level 3 rates. When our internal SMEs audited the payload, they found that the platform was sending “ea” instead of “each”. The platform adjusted their data going forward, and transactions started qualifying for lower interchange rates.

Simply sending Level 2 and Level 3 data often isn’t sufficient to qualify for reduced interchange rates. Someone needs to be monitoring the interchange rates to make sure that transactions are qualifying for the lowest possible rates and, if not, determine the root cause so the platform can make adjustments.

Our Platform Success team does this proactively.

Low cost competitors who are barely bringing in enough revenue to keep the lights on don’t have internal SMEs who can diagnose problems, let alone enough resources to proactively review interchange rates and drive optimization. Since interchange passthrough is by far the largest driver of payment processing costs, the opportunity to optimize interchange is often more impactful than the opportunity to reduce payment provider fees. This is especially true with B2B payments, where un-optimized interchange rates tend to be higher.

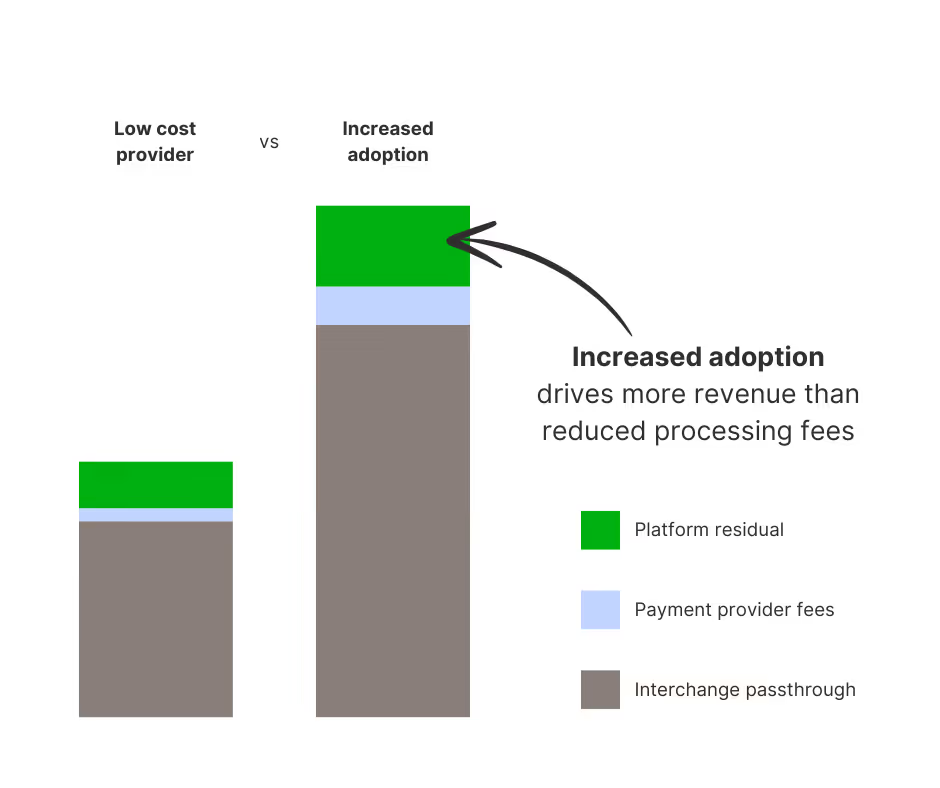

Poor adoption

For software companies looking to unlock enterprise value, payments adoption is the key. The core benefits of embedded payments (revenue, engagement, retention) are only realized if merchants actually use the payments product.

Low-cost payment providers have three issues that make it hard to maximize adoption.

- Low-cost providers can’t afford to invest in subject matter expertise or high-touch support, so they can’t guide software companies through the dozens of tiny decisions that make the difference between the blockbuster launch of a best-in-class payments product and the lackluster launch of an okay payments product.

- These providers tend to have nagging product issues, which makes it a lot harder to build a best-in-class payments product on a low-cost provider. It also significantly increases the software company’s support burden as the payment product grows.

- Low-cost providers tend to have longer response times to support requests, and often the support team doesn’t have the knowledge or authority to resolve the support request. This means software companies are telling merchants “we’re waiting for a response from our payment provider” and “our payment provider escalated to their vendor and we’ll let you know just as soon as we hear back”.

Saving a few basis points sounds great, but the long-term opportunity for higher adoption drives more revenue, profit, and enterprise value.

Holistic ROI is more important than cost

Many software companies weigh payment provider cost heavily because it’s tangible and directly comparable, where it’s harder to place a concrete value on support and product quality. On top of this, lower cost is generally perceived as less risky.

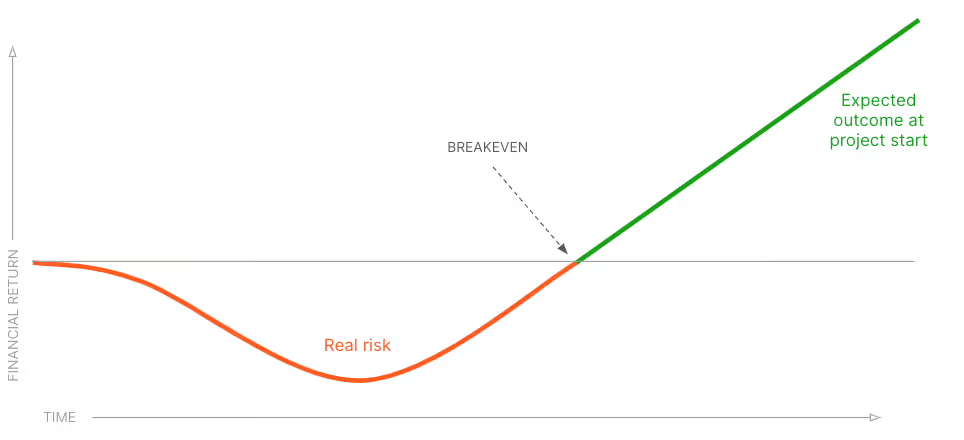

However, we’ve found that choosing a low-cost payment provider actually increases the risk of a failed payment project because all payment integrations cost resources to start, and the ROI isn’t realized until the processing volume reaches a tipping point.

Although the investment is slightly less with a low-cost payment provider, the likelihood of getting enough transaction volume for the payment project to pay off is a LOT lower. Product issues, slow or disempowered support, and lack of strategic guidance all hinder payments adoption and retention. With a low-cost payment provider, the software company is more likely to get stuck in the red part of the line graph above – where the payment integration is complete, but there isn’t enough volume for the software company to show ROI.

Most software companies find that it’s worth paying a little more to have a payments provider with robust technology that enables a winning merchant experience, and an expert support team that can help drive adoption and growth.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc